With the variations of product structures and features available on the market, it’s essential to have a nuanced process to making product recommendations to each individual client. While ratings and research software can be useful tools, it’s imperative to consider the individual values and need of the client in front of us and how to align the right kind of product to client profile.

How advisers can recommend the right product for a client – every time

Matching a product’s structure and features to a client’s risk profile and circumstances is always in their best interest.

Acting in the best interests of a client is a guiding principle for professional financial advisers, but sometimes a client’s ‘best interest’ isn’t immediately obvious.

A straightforward approach for advisers to fulfil these obligations is to align a product’s structure and features with a client’s risk profile and circumstances. This makes it clear to both your client and the regulator that you’re making an appropriate recommendation.

Defining your client’s ‘best interest’

As an adviser, you know you must put the interests of your client ahead of your own when you make a recommendation. It’s an obligation required by law under section 961B of the Corporations Act 2001 and highlighted twice in the Financial Planners and Advisers Code of Ethics under Standard 2 and Standard 5.

But from a risk advice perspective, what’s in a client’s best interest? Is it the most comprehensively rated product? The cheapest premium today? The cheapest premium over 10 years? Or none of these.

Both the law and the Code of Ethics use the overlay of appropriateness when making recommendations to a client. It highlights the importance of really understanding each of your clients and delivering advice that is relevant to their individual needs.

You should recommend the product that most clearly aligns to your client’s circumstances, even if it’s not the most highly rated or the one with the cheapest premiums.

How comfortable is your client with risk?

You also need to understand your client’s attitude to risk and their risk profile. Are they quite risk averse or risk comfortable? Different clients also vary significantly on what insurance solutions they’re willing to pay for.

To prioritise the right product features for a client, you need to understand which specific aspects of their lifestyle link to a particular product feature. You also need to have in mind any restraints on their capacity to pay.

For example, a risk averse client may value a solution that includes higher sums insured, age 65 benefit periods, own occupation TPD definitions, additional boosters and features and shorter waiting periods. Their aversion to risk means they are comfortable paying for the certainty of a comprehensive insurance solution.

A client who is more comfortable with risk may be content to compromise on sums insured, limited benefit periods, any occupation TPD definitions, less additional features and longer waiting periods. They are okay with retaining some level of risk (via self-insurance) and prefer putting their money to other goals.

Structure a product to align with your client’s goals

Decisions on product structure will tilt the ledger in the direction of either accepting additional risk or products with additional features and cost. By transparently outlining these trade-offs to clients and aligning them to the risk profile of the individual, you can provide a solution that’s most appropriate for their objectives. The table below sets out some examples.

*Benefits are often paid in arrears and an additional buffer may be required.

Do individual features suit your client?

The individual features of a product can also help you align the right recommendation to the right client. You should consider:

• Future insurability

Products that include future insurability may be valuable for clients who are likely to have additional needs in the future – making medical underwriting-free increases an important tool for long term planning.

• Waiting period requirements

Definitions of this requirement can vary a lot. Some products have requirements for up to 14 consecutive days of total disability to access a claim; others have no total disability requirement during the waiting period and the ability to access partial disability on day one. Understanding your client’s expectation can help you narrow a choice to the most appropriate product.

• Additional boosters/ accident benefits

Some clients may be particularly concerned with early access to benefits, or access to additional early amounts after an accident or trauma event. A product with these features can facilitate this and deliver value for money for your client.

• Total and Permanent Disability (TPD) definitions and waiting periods

Beyond ‘own occupation’ and ‘any occupation’ definitions, (which you should align with a client’s occupation and work history) different products may include longer waiting periods to claim on TPD. There may also be additional tiers to access TPD payments for events such as loss of limb or sight/hearing. Understanding a client’s expectations can help you align these to the right client profile.

• Trauma inclusions

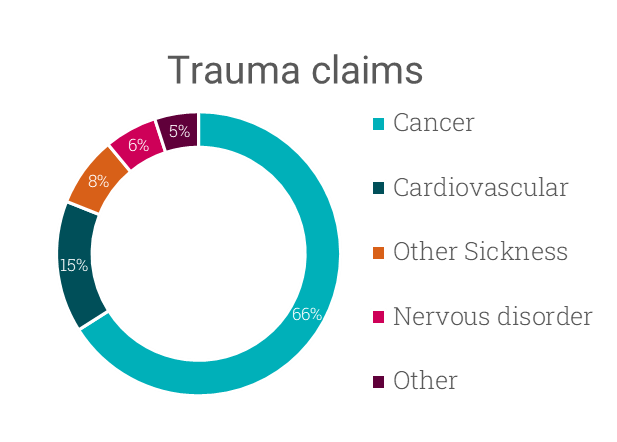

It’s important to educate clients so you can discuss what’s suitable for them. For trauma insurance, this can include access thresholds for degenerative conditions claims, if a condition will only be covered by or a full or partial claim, or the list of simple diagnoses that are covered. It’s important to consider whether payment is subject to severity criteria or triggered by diagnosis only. Data on claims statistics (such as the MLC Insurance 2022 numbers below) could assist when reflecting on what’s important.

MLC Life Insurance Trauma claims: January – December 2022

•Buyback / reinstatements

Different products may have buyback or reinstatements. These can sometimes be built into the product or be an extra cost option. When exercised, the bought-back or reinstated product may differ on what’s excluded for subsequent claims. Talk with your client about what they expect from regained cover and what they could claim on, and if this future coverage is important.

Informed clients make better decisions. By having these discussions, and truly getting to the heart of what is important to the client, advisers can show the real benefit of professional risk advice. It goes beyond finding the highest rated product or cheapest premium.

By better understanding your clients, you can get their buy-in long term. You may also create advocates who will promote your services to friends and family. And you’ll seamlessly meet your compliance requirements to act in a client’s best interest.

Learn more about aligning products to your client’s needs in Marshall Ross’s two-part webinar series. Reach out to your dedicated BDM to learn how to access on-demand webinar recordings.

Register here.