In this special production

About this paper

This paper has been prepared by Ensombl as a resource for financial advisers, with the permission and support of Allianz Retire Plus.

We would like to thank the following adviser contributors

Retirement Incomes Philosophy

The need for a Retirement Incomes Philosophy

The Investment philosophy is a foundational concept within financial advice. By distilling a firm’s core investment beliefs and processes into a documented approach to investing, advice practices are able to deliver a complex, tailored service with more consistency, efficiency, and transparency.

An insurance philosophy is an equally powerful concept, wrapping up processes around product selection, premium funding, sum insured calculations and risk management in an overall approach that can be applied consistently to every client scenario.

It is perhaps surprising then that, until now, the concept of the Retirement Income philosophy has received little, if any, attention.

Retirement planning is already the most dominant advice sector, with research1 by Natixis Investment Managers, which found around 90% of Australian financial advisers are focused on servicing individuals between 50 and 60 years of age, namely pre-retirees.

It is also arguably the most intellectually demanding sector of financial advice, involving a complex and constantly changing regulatory overlay, a myriad of rules around superannuation, Centrelink, and aged care, a widening choice of product solutions, and the complexities of estate planning and intergenerational wealth transfer.

But while Australia’s compulsory superannuation regime is rightly regarded as being among the world’s best2 in terms of helping people accumulate retirement savings, too little focus has, to now, been directed towards the decumulation of those savings.

The paucity of product offerings and guidance frameworks to help retirees optimise their retirement incomes – and indeed their retirement lifestyles – has been recognised as a major policy gap, one which the 2022 Retirement Income Covenant is intended to address.

The imperative in addressing this gap is seen in the numbers of superannuation members who are in, or will soon enter, the decumulation or retirement phase.

Between 2015 and 2022, the number of member accounts in retirement phases grew to over 1.3 million people3. Over the same period, the value of member benefits in retirement phase grew from $247 billion to $478 billion, an average annual growth rate of 10%.

With the Australian Bureau of Statistics (ABS) estimating around 700,000 Australians will retire between 2023 and 20284, it is clear that the number of people who will switch from accumulating to decumulating retirement savings will surge.

If advisers are to play their central role in facilitating an optimal retirement incomes system, then their ability to develop retirement income strategies efficiently, consistently, and transparently, is paramount.

The time for the Retirement Income Philosophy concept to become mainstream is therefore now.

What should a Retirement Incomes Philosophy address?

As with investment and insurance philosophies, retirement income philosophies will reflect the unique beliefs, methodologies, and business model of each individual practice. Within this continuum though, the following components – reflecting the major situational challenges of retirement income strategy – are likely to form the core:

- The nature of risks faced by retirees, including the unique financial risks associated with decumulation, and the emotional challenges associated with retirement

- Processes for assessing and quantifying those risks (recognising that risk profiling methodologies used for accumulation clients are likely to be unsuitable)

- Methodologies for designing and implementing retirement income strategies and portfolios, and

- The toolkit of product solutions that can be called upon to bring these strategies to life.

Adviser insight – a retirement philosophy is efficient

Just like an investment philosophy and an insurance philosophy, a retirement philosophy should link back to the types of strategies and products you will call on, so you aren’t reinventing the wheel for every new client. Warwick Abbott.

SECTION 1 —DECUMULATION BRINGS FORTH DIFFERENT RISKS

The objectives and strategies applicable to the accumulation phase of retirement savings are different to those applicable to the drawdown – decumulation – phase. Similarly, the risks faced during decumulation are significantly different, and simply applying a more conservative investment approach is likely to lead to sub-optimal outcomes for the individual.

Decumulation is not accumulation in reverse.

While the miracle of compounding is arguably the main driver of retirement savings outcomes over a person’s working life, decumulation brings forward a number of forces that can significantly interrupt this compounding. These forces are significant risks to be managed, and include:

- Dollar cost averaging is no longer an opportunity, it’s a threat. Regularly selling assets to deliver consistent income flows will mean some assets will be sold when the market is down, leaving the investor to either sell more assets, or have a lower income to live on

- Liquidity considerations are elevated. A portfolio designed to deliver a sustained income over decades will likely need to balance the higher earnings potential of more illiquid assets with the liquidity required for planned and unplanned drawdowns

- The stakes are higher, particularly in the early stages of decumulation, when the savings pool is at its peak

- There are less opportunities to recover, especially for those who retired several years ago, and for whom returning to the workforce is more difficult

- Behavioural risks intersect with market risks to increase the chance of an individual crystallising losses during market dips.

Adviser Insight – inability to recover drives conservatism

Clients will say to me “I can’t afford to get this wrong, as I can’t go back and start working again”, so it’s no surprise that gives them a defensive mindset from the beginning. Warwick Abbott.

The financial risks faced in retirement

While all investors face varying degrees of market risk – the risk of losing money when the market falls – retirees drawing on their retirement savings face additional risks that must be mitigated:

Sequencing risk and the Retirement Risk Zone

Sequencing risk is related to the sequencing, or timing, of market falls relative to the time of retirement. Investment markets are notoriously unpredictable, and any market falls either just before or just after retirement – when retirement savings are at their peak, will have a proportionately greater impact, because there is less time to recover before withdrawals commence, and because the dollar value of any loss will be at its maximum.

Often referred to as the Retirement Risk Zone5, many experts see this critical period – when market conditions can have the most impact – as the 7 years just before and after a client retires.

The impact of sequencing risk can be significant. With some estimates suggesting that as much as 60% of every dollar of retirement income comes from the investment earnings you make in retirement6, the consequences of starting retirement with a lower balance will be felt throughout retirement.

The likelihood of running out of funds is obviously increased, which can lead to people deferring their retirement. On the flip side, some may feel compelled to take even more investment risk in order to reach their retirement savings goals (but which exposes them to the chance of higher losses).

Longevity risk

The most fundamental risk, which manifests as most retirees’ greatest fear, is that a person will outlive their retirement savings.

As life expectancies continue to improve, longevity risk is also heightened.

In Australia, a 65-year-old male would expect to live another 20 years, and females another 23 years7. For a retiree couple aged 65, there is a high statistical probability that at least one of them will survive beyond age 90, meaning a retirement savings pool may need to be drawn upon for 25 years or more8.

With ATO analysis from 2021 finding the median superannuation balance for those aged 60 – 64 was $211,996 for men and $158,806 for women9, longevity risk clearly looms large for many Australians, and a reliance on the government age pension is almost inevitable.

Adviser Insights – longevity risk dominates retiree thinking

Running out of money (i.e., longevity risk) is a key concern which can prevent some retirees from spending with confidence, especially early on in retirement. Philip Hall.

If I had to rank the risks clients worry about, longevity risk would definitely come out on top. David Leslie.

Where people are most uncertain is around the longevity of their wealth, and what their wealth can provide. Warwick Abbott.

Inflation risk

Inflation poses a risk to retirees in two ways.

Firstly, the erosion of spending power, as experienced through the post Covid19 inflation spike, means retirees need to make bigger drawdowns from their retirement savings to maintain the same lifestyle. Unlike those still in the workforce – who can hope for some sort of inflation-linked salary increases – keeping pace with inflation generally means drawing down on funds more quickly, accelerating their depletion.

Secondly, inflation isnt experienced uniformly. Some categories of goods and services experience higher rates of inflation than others. Retirees household consumption of clothing, groceries, healthcare, energy, housing and beverages is likely to differ to young couples, or families.

Healthcare inflation notoriously runs above headline inflation on a regular basis, disproportionately affecting those in poor health. Figures for the year ended 30 April 2024, for example, showed annual healthcare inflation running at 6.1%, compared to the 3.6% increase in the overall Consumer Price Index (CPI)10.

In the midst of the 2022 inflation surge, Head of Prices Statistics at the ABS, Michelle Marquardt, said11:

“Living costs for Age Pensioner households have been particularly impacted by increases in food and non-alcoholic beverages, as grocery food items make up a higher proportion of overall expenditure for Age Pensioner households compared to other types of households.”

In effect, retiree inflation can sometimes be higher than that for working households.

Tax risk

With a finite retirement savings pool, any avoidable drawdowns come into sharp focus.

Tax is understandably a key focus of retirement advice, with the navigation of complex assets and income tests, superannuation tax rules, and gifting guidelines almost impossible for the un-advised.

One recently reported example of tax risk is the high proportion of people over 65 who have kept all their superannuation in accumulation mode, thus ensuring their entire balance remains subject to the 15% tax on earnings.

According to 2022 APRA data, around half of all over 65 members in APRA regulated funds were still in accumulation mode12. While a proportion of these may still be working, or have otherwise valid reasons for staying in accumulation mode, it seems likely the majority are effectively allowing tax to erode their retirement savings unnecessarily.

Spiking expenses risk

This is the risk of large unplanned expenses, the magnitude, frequency, and timing of which cannot be predicted.

These could range from major home repairs, health related expenses either for the retiree or their loved ones, or even ‘grey divorce’.

The emotional challenges of retirement

Retirement throws up many psychological challenges, and unsurprisingly, many advisers working with retirees find their role in providing emotional support and non-financial guidance is just as important as the financial advice they give.

The loss of income, social contact, and routine can prove daunting for many, especially those whose retirement was unplanned (perhaps due to redundancy or ill health).

People who have long, successful, enjoyable careers may suddenly find they lack focus, or even purpose, and may have diminished self-worth. Boredom can easily creep in, and mental health can suffer.

A perceived loss of financial independence and fear of being a burden on others can also loom large.

Adviser insight – loss of certainty around purpose is a challenge

Retirement is not just about the loss of certainty around income, it’s about the other things that sustain you, the hobbies, the social connections, the sense you are making a positive contribution. I’ve always thought psychology should be a part of financial planning studies, and working with retirees and pre-retirees has just reinforced that belief. David Leslie.

I try to unpack what makes people happy, gives them a sense of purpose, and helps them stay connected to a community. It’s important that, if there are two individuals involved, both are given a voice in the conversation, so they both feel heard. Warwick Abbott.

Adviser Insight – financial risks and internal risks

I see 10 retirement risks. The 5 external ones everyone talks about, longevity, sequencing, market, inflation, and taxes, plus the internal ones which include fear of running out and the unnecessary frugality that can result, lack of discipline, which can see overspending, structure, and issues relating to the unpredictability of family situations, such as adult children and gifts and early inheritances. Then the ripple effects of all these. Vince Scully.

Grey divorce is costly, and on the rise

The sudden and significant change in routines can also see relationships can come under strain.

Indeed, research13 released in 2023 found that while overall divorce rates have been falling from their 1990s peak, divorce rates in the over 50s have bucked the trend, and around a third of all divorces are taking place after the age of 50.

The financial consequences of divorce in retirement can be devastating, with the potential for large legal fees to eat into retirement savings, as well as the loss of expense sharing ability that makes life more costly for singles.

Loss of certainty is the biggest risk

Almost universally, the biggest emotional challenge faced by retirees – those in decumulation mode – is the loss of certainty around their income.

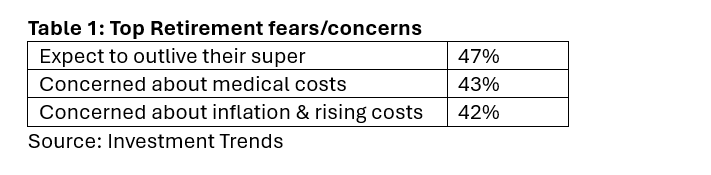

2022 research by Investment Trends14 found that expectation of outliving their superannuation savings was the top fear/concern for Australian retirees:

Loss of financial certainty is more than just longevity risk, it is actually the combination of statistical longevity risk with a loss of psychological safety, which manifests as an extreme conservatism in risk appetite, and heightened loss aversion.

Adviser Insight – clients look to advisers for certainty

Clients face so much uncertainty in retirement, about their lives, about their finances, about the right path through and the tools to use. They look to us to provide certainty through our professional judgement. That obviously relies on a foundation of trust. Mark Spagnolo.

The risks of becoming too conservative

Without expert advice, this conservatism can see retirees live unnecessarily frugal lives, taking the joy out of retirement. It can also see them take overly defensive investment positions, robbing them of the growth their portfolio needs to sustain a multi-decade income stream.

Worse still, it can become a significant behavioural risk, increasing the likelihood of selling down growth assets in panicked reaction to market downturns.

Adviser insight – a conservative attitude is at odds with reality

There’s no doubt clients tend to adopt a more conservative attitude simply because they are about to retire, but then I point out to them that if they are 60, they may still have a potential investing timeframe of 30 years or more. Philip Hall.

The theory says when you are in pension phase you need to de-risk and move towards more conservative investing, but that can be very much at odds with the reality of people needing to generate income, for as much as another 3 decades. David Leslie.

Adviser Insight – we need to create the psychological safety to spend

The biggest psychological hurdle in retirement is that transition from believing ‘saving is good, spending is bad’, to ‘spending is good, but just not too much’. Creating the psychological safety to spend is the key to getting the retirement piece right. Vince Scully.

Data shows the shift to defensiveness at retirement

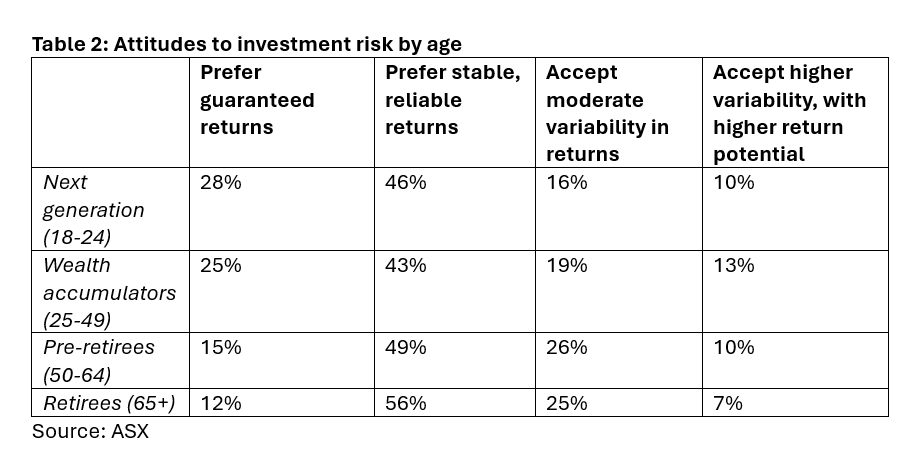

Research15 for National Seniors found that around 70% of pre-retirees said their investment strategy would become more conservative, or somewhat more conservative, at retirement.

Similarly, the 2023 ASX Investor Study16 found that retirees ranked highest for seeking ‘stable, reliable returns’, and ranked lowest for accepting ‘higher variability with potential for higher returns’.

SECTION 2 —A NEW APPROACH TO ASSESSING RISKS IN RETIREMENT

Different risks demands a different approach to risk profiling

To the extent that the decumulation brings forth a unique set of risks not relevant to accumulators, the assessment of these risks requires a different approach.

There are a number of reasons why the techniques used to assess risk for accumulators are inappropriate for decumulation scenarios:

- They often concentrate more on attitude to risk more than risk capacity

- Many questions don’t make sense in a decumulation scenario, being focused on reaction to portfolio losses rather than the changes in the size and stability of income flows

- They really just help decide how aggressively someone can be invested in equities, they don’t help differentiate between appropriate strategies and products

- They don’t reflect the fact that the separation seen between an accumulator and their portfolio no longer exists in decumulation, where those investments are now being accessed regularly, and that behavioural risks are therefore higher

- They are often done infrequently, meaning they don’t reflect the dynamic nature of risk.

Risk Tolerance v Risk Capacity

In most instances, Risk Capacity – the financial ability to absorb losses – is the chief determinant of the suitable level of risk for an investor to take. But the experience around the world – likely to be replicated in Australia – is that many risk assessment processes conflate risk tolerance (psychological attitude to risk) with risk capacity, despite the fact they should be assessed separately.

In the UK for example, a recent study by the financial regulator (FCA) found only 30% of advice firms were using separate processes for assessing the two17.

Further problems can occur with risk capacity assessments that are subjective guesses, or which focus on pots of money – each with their own arbitrary goal – and fail to reflect how an investor’s goals interact with each other over time.

Poor – or absent – risk capacity assessments can lead to an investment approach which is either too aggressive, increasing the risk of knee jerk investor behaviour, or too conservative, threatening the sustainability of income flows.

Adviser Insight – Risk capacity the more important metric in retirement

For retirees we would look to emphasise capacity for loss over tolerance for loss. When you are 20 or 30, what matters is your risk tolerance. But when you are 55 or 60 or older, your capacity for loss becomes more relevant, and those who don’t necessarily lead you to the same place. Vince Scully.

Inappropriate questions

Accumulation strategies are generally singular in their focus: to maximise the total investment returns achieved in order to grow a portfolio as much as possible.

Investors are generally advised to invest as aggressively as possible to earn the greatest risk premium from the stock market over the long-term, subject to their comfort with short-term market fluctuations (that will hopefully balance out into a greater growth rate over time).

Traditional Risk Tolerance questionnaires have thus been designed to help advisers identify the amount of volatility their clients can stomach within their investment portfolios – which is likely to be quite different to their attitude to income stability or certainty.

Whereas for accumulators, questions about whether risk is something to be feared, or an opportunity for upside, are likely to be relevant, for decumulators, questions designed to measure sensitivity to loss will make more sense.

The same FCA study referred to above found that 77% of advisory firms used the exact same process and questions for assessing the risk attitudes of both accumulators and decumulators18.

Adviser insight – traditional risk profilers geared towards younger accumulators

I think the outputs from some traditional risk profilers can be shallow and one dimensional, and predicated on questionable underlying academic and philosophical assumptions about the type of investor who seeks growth. David Leslie.

Adviser insight – multiple tools to measure behavioural risks

Alongside the traditional investment risk profiling, we use our own money personality test, which looks at 13 attributes of why you do what you do with money, including trust, willingness to delegate, belief in hard work, belief in luck, and altruism. That allows us to classify people into one of nine money personalities. Two of those will reduce your stated risk preference. Vince Scully.

They don’t help determine strategy

Traditional risk profiling outputs are designed to help advisers match the allocation between growth and defensive assets to an individual’s risk tolerance. And notwithstanding the growth of alternative investments, growth assets are largely seen to be direct equities, or equity-based products (managed funds, ETFs, SMAs).

The sequence is usually (1) determining the asset allocation and (2) deciding the right products.

For retirees in decumulation mode however, there are so many different product solutions – catering for different client needs for flexibility and certainty – that the sequence needs to be reversed, with the choice of strategy (including the use of different types of annuities and new innovative income stream products) needing to be made before any asset allocation decisions.

A suitable risk profiling approach in decumulation should therefore help shed light on the appropriate strategy and product selection.

Lack of separation understates behavioural risks

Accumulators are generally making long term investment decisions about assets they don’t intend to access for some time. As such there is a degree of psychological separation from these funds that likely manifests as a higher risk tolerance. This is especially true of superannuation funds, which are inaccessible until age 60, and therefore for many investors don’t feel ‘real’.

In decumulation however, individuals become more engaged with their savings, needing to access them and make decisions about them on a far more frequent basis. Increased loss aversion is natural for retirees, but often one’s true attitude to losses isn’t known until a loss is experience. Risk profiling processes geared around accumulation may therefore underestimate an individual’s true aversion to loss, leading to increased risk of value destructive behaviour.

Adviser Insight – lack of retiree engagement with their super creates uncertainty

Most people don’t engage that much with their super, and they arrive at retirement not feeling in control and not appreciating what it is capable of, or the range of assets we could utilise to support their income. David Leslie.

Risk is dynamic, not ‘set and forget’

Attitudes to, and capacity for, risk are dynamic, evolving over time in response to changes in an investors circumstances and goals. Changes in income, employment status, health, relationships, and living arrangements can all impact a person’s capacity and willingness to take investment risk.

The reliance on an initial risk profiling process to remain accurate throughout a client’s life is therefore highly misplaced.

Adviser insights – risk profiling needs to be done regularly

For clients eligible for the age pension, the whole make up of their asset pool and income flows will change, and for that reason alone, risk profiling needs to be revisited at or near retirement. There are a myriad of other reasons too. Vince Scully.

Risk is dynamic. People can have things going on personally that can affect the way they respond to something. Even their capacity to take risk can be different at times throughout the year. Mark Spagnolo.

We check their risk profile at least every time we have a review, either through a formal process or through conversations about what’s going on in their lives, to see if there are any inconsistencies or signals of any changes that might affect their capacity. Warwick Abbott.

It’s good practice to review client’s risk profile regularly. If it’s more than a couple of years old, even without any obvious major changes in their lives, you should still go through the process again. David Leslie.

Adviser Insight – risk tolerance can change in a way you don’t expect

Clients who have been conservative during the accumulation phase may actually become more risk tolerant over time, as they become more educated, which is why it’s important to regularly re-assess their tolerance and capacity. Mark Spagnolo.

A best practice approach to measuring attitude to risk in decumulation

There is much scope for an improved approach to retirement income strategies in Australia (a fact called out by ASIC and APRA in their 2022 Retirement Income Covenant (RIC) Review), and a valuable starting point is to look to the experiences of other similar developed markets, namely the UK and USA.

Gauging the need for certainty

Internationally recognised US retirement planning academic – Professor Wade Pfau – is one of many experts who believe a new approach is needed to (1) assessing retiree attitudes to risk and (2) developing retirement income strategies aligned to those risks.

His latest work in this area is the Retirement Income Styles Awareness (RISA) Profile19.

The RISA profiling tool was after years of research by Pfau and colleagues, which identified retiree attitudes towards funding essential living expenses as one of the key determinants of their retirement income ‘style’.

The tool maps retirees along two dimensions:

- Safety first versus probability, and

- Optionality versus commitment.

The ‘safety first versus probability’ dimension is about where a retiree expects their retirement income to come from. Are they seeking a turnkey ‘pay cheque replacement’ for their retirement, or are they happy sourcing income from a total return portfolio even if that might entail some variability in income flows?

Adviser Insight – feelings, not numbers, a better measure of income risk attitudes

Some people don’t know how to even answer some of the normal risk profile questions, and they try and get very analytical. That’s why I always try and bring things back to feelings – ‘how would you feel if this happened. And if you are fearful, how would you behave in those circumstances’? David Leslie.

Questions to determine Retirement Income ‘styles’

The first question aims to gauge your views on how you expect to fund your retirement income

An example of a question to assess this dimension is:

Which of these two statements most closely reflects your views on retirement income planning?

• “I see my investment portfolio as funding the majority of my retirement expenses.” OR

• “I see my essential retirement expenses funded, to the extent possible, from protected income sources, with the rest of my expenses funded by my investment portfolio.”

A second question then seeks to gauge a retirees’ preference for a flexible approach, versus the certainty that comes from committing to a particular strategy throughout retirement.

An example of a question for this dimension:

How much do you agree with the following statement?

“I prefer more flexible retirement income strategies to accommodate my changing preferences as I age”

The responses to these and other questions in the RISA profiling tool allows individuals to be mapped to one of 4 retirement income strategy quadrants. The strategies underpinning these quadrants are similar in nature to those used by Australian advisers, albeit with different labels, and are further explored later in this paper.

Adviser insight – a localised variation on the income styles assessment

We have a four-quadrant matrix we use with our clients, designed to gauge their feelings about their freedom of choice and sense of security – a variation on flexibility and certainty – both in the present and the future. Their feelings in each of these areas will change, so for example higher inflation will impact their sense of security. This is where we can see if there is anything we need to change or work on, potentially involving a flexibility trade-off in return for bringing the sense of security back. Warwick Abbott.

Adviser Insights – the first question should be about income source

The initial conversation I would have with a client, would be where they wanted to source their income from. From rental income, from dividends, from interest, from investment returns? The answer to that question, in combination with their risk profile, gives you a starting point to build a strategy. Philip Hall.

Other questions to gauge attitudes to income risk

The previously mentioned FCA review of retirement income advice in the UK spurred a flurry of work and commentary around income risk, and its foundational importance in developing retirement income strategies aligned to individual needs and attitudes.

Commentary also focused on the development of questions more suitable for assessing attitudes to income risk, rather than investment risk.

Even subtle changes to the questions used in accumulation can make a significant difference.

For example, in accumulation it may be appropriate to ask a client whether they are willing to take more risk in the hope of higher returns. In decumulation, it might be more relevant for the client to consider whether they value a stable lower income, or would rather take more risk in exchange for the potential for higher, but also more variable, income.

Similarly, in accumulation it makes sense to ask whether a client seeks risk as something to be feared, or an opportunity for upside. In decumulation it is more appropriate to measure sensitivity to loss.

It may also be appropriate to tweak the client fact find used with pre-retirees, or at the very least look at the outcomes through a different lens.

Questions such as:

What are your daily living expenses?

- Do you have a cash buffer to cover unexpected expenses?

- Do you have dependents that rely on you for money?

- Are your income requirements likely to change in the future?

- Do you have any large expenses planned?

The more closely income is linked to client’s day-to-day life, the more important income stability is likely to be.

Adviser Insight – desired lifestyle a lens through which to assess risk

I think the more interesting, more valuable conversation to have is about the type of lifestyle do they want to have. The projects they want to complete, the travel they want to do. That then sets up a conversation about risk and certainty trade-offs that is more realistic. Philip Hall.

Use of cash flow modelling for risk capacity assessment

In Australia, cash flow modelling is typically thought of as a form of advice – typically used with younger clients – rather a risk modelling tool. But in the UK, cash flow modelling is seen as a primary tool for assessing capacity for risk.

Experts agree a diligent and comprehensive cash flow model is the most accurate way to assess risk capacity, with the ability to model the income effect of different degrees of investment loss central to this calculation.

As part of its thematic review of retirement advice, the Financial Conduct Authority recently published guidance on improving the quality of cash flow modelling for retiree and pre-retiree clients. Areas they highlighted for improvement included verifying the accuracy of client provided data, and using realistic return assumptions20.

Another problem identified in the FCA review was the common use of ‘average’ life expectancy (rather than adjusted), and the failure to stress test different outcomes in line with different investment return scenarios.

As the importance of, and regulatory spotlight on, the retirement income sector grows, the use of cash flow modelling for retirees and pre-retirees is likely to become more common.

Adviser Insights – cash flow modelling using client’s bank data feeds

With the client’s approval, technology gives us the means to access their spending data and prepare fairly detailed cash flow modelling, so we can monitor and adjust their plan accordingly. Warwick Abbott.

Adviser insights – the risk of underestimating longevity is real

Advice clients as a cohort are likely to have higher incomes and lead healthier lifestyles than the population overall, meaning they are statistically more likely to have an above average life expectancy, by which I mean low or even mid-nineties. That can change your calculations significantly. Vince Scully.

Some clients are what you might call genetically blessed in that they have a family history of longevity. That can play into their own sense of longevity risk and also their attitudes to annuity type solutions. Philip Hall.

SECTION 3 —RETIREMENT INCOME STRATEGY CHOICES

Retirement income strategies

There is a wide variety of income strategies used across the market, with an equally wide variety of labels attached to these strategies.

Terms like ‘layering’ and ‘bucketing’ are heard frequently, although the definitions applying to the terms aren’t always consistent.

Common strategies

A range of strategies is used across the marketplace, each varying in their complexity, ability to mitigate the unique risks of decumulation, and degree of personalisation.

Ranked in order of complexity and personalisation (lowest to highest), these include:

- The same strategy & asset allocation as used in accumulation

- A more conservative allocation

- Simple bucketing

- Complex bucketing

- Income layering.

What is Bucketing?

A bucketing strategy aims to help balance the need for ongoing income and capital growth throughout retirement by establishing and maintaining different pools of savings, each with their own purpose and liquidity needs. The aim is to generate capital growth while reducing the risk of having to sell investments when the market is down.

There are many variations, but a simple bucketing strategy might have three buckets:

- The short-term bucket. The liquid component from which your income is drawn. Invested for stability not growth and therefore immune from volatility.

- The medium-term bucket. Balances need for stability with potential for medium term capital growth.

- Long term bucket. Invested for long term growth, designed to mitigate longevity risk.

Positive returns from the long-term bucket are used to top-up or repair the short-term bucket. If the market falls, the aim is not to sell from this bucket.

Complex bucketing strategies would involve more buckets, more tailored to specific financial objectives, and with a more dynamic top-up or repair process.

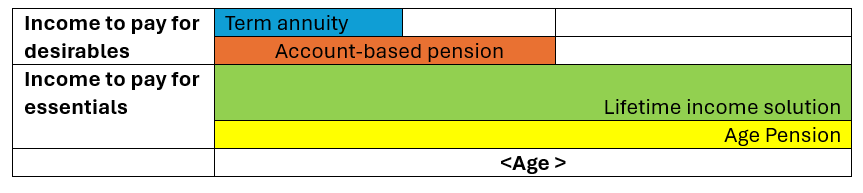

What is layering?

Whereas bucketing is more of an asset allocation strategy, layering is more dependent on different product solutions to deliver different layers of income.

These layers could include:

- The basic layer, which is about essential expenses (food, housing, utilities, transport)

- The contingency layer, which is about unexpected expenses, such as healthcare or home repairs

- The discretionary layer, which funds the nice to have assets and activities, and

- The legacy layer, to leave funds for family.

Product solutions typically supporting these strategies can include the age pension, account-based pension, term annuities and lifetime annuities (as well as the new era innovative income stream products).

Adviser insight – layering income sources is also a form of diversification

Diversification of income source can be as important as asset diversification, and where appropriate I will put in place layers of income that are a little bit uncorrelated. Mark Spagnolo.

Adviser Insight – a different kind of layering to help achieve certainty

A strategy I have used in the past is to layer multiple lifetime annuities, some of which can be cashed out if absolutely necessary. You have the income certainty, but the clients have comfort that they haven’t completely locked away their funds. Philip Hall.

Towards more retirement-risk aware strategies

The outputs from the Retirement Income Styles Assessment are based on a broader conceptualisation of risk as it pertains to income preferences and risk tolerance.

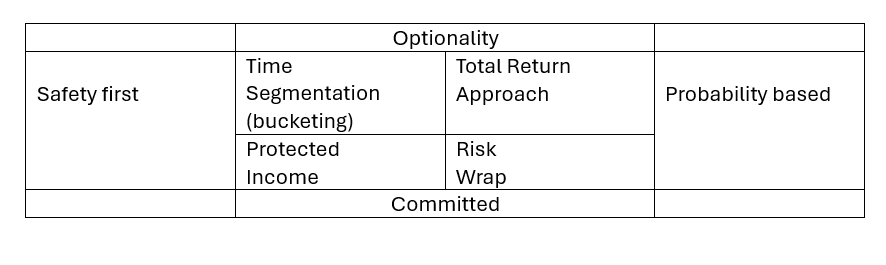

Mapping individuals along two dimensions (optionality v commitment and safety-first v probability) allows them to be aligned with one of four retirement income strategies, described below.

Protected income approach. This allows for immediate and deferred annuitisation to support greater downside spending protection and building an income floor to cover essential expenses.

Risk wrap approach. This blends investment growth potential with lifetime income benefits, through an annuity and/or innovative income stream product. Such tools can be designed to offer upside growth potential alongside secured lifetime spending, even if markets perform poorly. This provides a protected source of lifetime income as part of the overall investing strategy.

Time segmentation or bucketing approach. As already described, this approach offers protections without sacrificing flexibility. Money is divided into different categories, earmarking assets for spending immediately, soon, and later. The longer-term portfolio can gradually replenish the short-term buckets as these funds are spent.

Asset allocation decisions are made after the strategy is selected.

Using the income-styles approach in Australia

While the RISA tool has been developed in the USA, the theoretical underpinnings are equally applicable in other markets, and with the exception of questions relating to US specific products and legislation, the questions used in the assessment are just as relevant in an Australian context, whether used in conjunction with the RISA tool, or on a standalone basis.

SECTION 4 —RETIREMENT INCOMES PRODUCT TOOLKIT

New product solutions to bring retirement income strategies to life

Most advisers call on a small core of established, widely available product solutions to support the retirement income strategies they design for clients. Typically, a strategy will involve a number of solutions working in conjunction to deliver different objectives within that strategy.

For example:

Outside the superannuation system, the solutions called on by advisers will typically include those offering liquidity (such as cash and fixed interest) and those offering access to equity markets, including ETFs.

Traditional retirement income solutions

Annuities are used for a variety of purposes, either as de facto term deposits (term annuities), or to create a degree of income certainty (lifetime annuities).

Lifetime annuities are available inside and outside the superannuation system, and this is a class of product getting more sophisticated, with CPI and market linked solutions available. The lack of flexibility in lifetime annuities can, however, be a barrier for some.

The Account-Based Pension (ABP) remains the most common decumulation solution for superannuation savings, and again, these offerings are becoming more sophisticated.

Next era innovative income streams

Next/new era retirement income solutions are a new style of retirement incomes product, enabled through legislation, and designed to provide consumers with greater choice and flexibility when considering their retirement product options, helping them manage the risk of outliving their retirement savings and enhancing their standard of living in retirement. As explained below, they are designed to overcome some of common objections consumers may have to traditional lifetime income stream products.

ABPs alone do not mitigate the key retirement risks

The flexibility of ABPs means they can work very well in conjunction other solutions, such as the Age Pension and annuities, and subject to mandatory minimums, can be integral to a dynamic drawdown strategy. However, they are not in themselves, a mitigant against sequencing risk, inflation risk, or longevity risk, and as such offer no income certainty to retirees.

Adviser Insight – layering in a guaranteed floor can allow you to dial up the risk

Using a lifetime annuity can open up the door an age pension sooner, and adding that guaranteed income floor means the client could take more risk if they wanted to. Warwick Abbott.

Traditional solutions offer flexibility or certainty, not both

Today, more than ever, retirees want the confidence to spend and enjoy the continuity of their lifestyle. For this, they need certainty and flexibility from their investment strategies, as well as solutions to the unpredictable financial outcomes they’ll likely face in retirement.

At one end of the spectrum, account-based pensions provide flexibility but can leave retirees shouldering significant investment and longevity risk and fail to fully address the financial fears held by retirees.

At the other end, traditional lifetime annuities involve trade-offs between income certainty and flexibility and are often limited in terms of how one can invest, withdraw or use their money.

The Age Pension, upon which many Australians rely once their retirement savings are exhausted, barely provides enough income to sustain a subsistence level of retirement.

As life expectancies increase and living costs rise, the strategies and products previously relied upon are becoming less effective in addressing the need for certainty.

With the retirements of 4.2 million plus Australians210 at stake, the imperative for advisers to turn to new era retirement income solutions has never been greater.

Next-generation retirement income solutions can provide certainty and flexibility

A 2022 Actuaries Institute report22 noted that combining traditional products with innovative solutions could lead to a remarkable 30 percent increase in retirement income.

Further, the report noted that methods, such as using investment-linked lifetime income streams, have been shown to lift retirement income without increasing longevity risk: a win-win outcome that would see Australian retirees benefit from larger payments and a better quality of life without increasing the likelihood of outliving their savings.

The next generation of retirement products must improve on earlier efforts, with outcome-oriented solutions designed around core features, including:

Adviser insight – innovative income streams and the best of both worlds?

The new style of retirement incomes product potentially give you the best of both worlds – they give you the floor, through their Centrelink treatment, and that allow you to have some market upside, so there’s a lot to potentially like. Vince Scully.

Adviser insight – more levers and better outcomes in the flexibility trade-off

As an adviser is good to see some innovation. With traditional products, you could trade-off flexibility for guaranteed income flows that weren’t necessarily that impressive. With the newer products you have options like deferral periods and downside protection, you just seem to have more levers to pull, which makes it easier for advisers to tailor to the client and the circumstances. Mark Spagnolo.

Bringing forward the retirement incomes conversation

It is generally accepted that the earlier one starts planning their retirement income approach the better. All the advisers interviewed for this paper agreed that while an ideal ‘runway’ was at least 10 years out from retirement, in reality many clients were not seeking advice until much closer to retirement, making it more challenging to design the optimal strategy.

The design of new era income solutions is intended to encourage and reward individuals for implementing retirement income solutions much earlier (while still in accumulation phase).

This creates an opportunity – and an incentive – for advisers to bring forward their retirement income planning conversations with clients.

New era solutions in action: Allianz AGILE

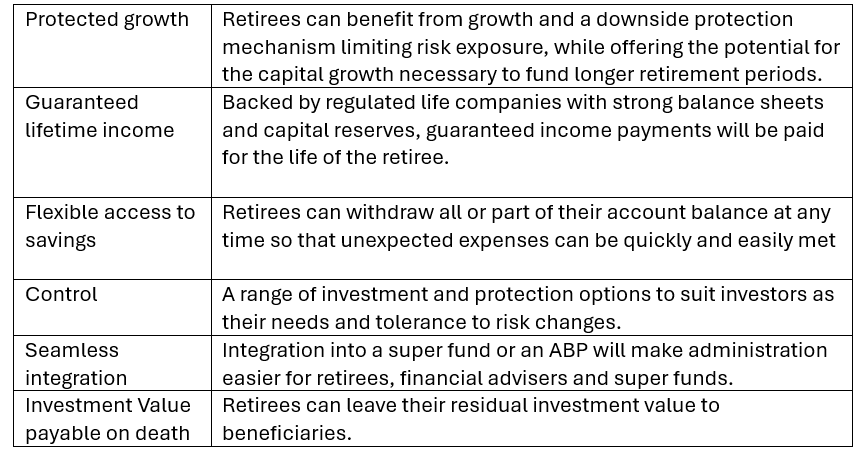

Allianz Guaranteed Income for Life (AGILE) is one such new generation retirement income stream solution, delivering certainty in the form of a guaranteed income for life – and it has the potential to transform retirement.

AGILE provides the certainty that comes from combining a protected investment with the potential for performance growth with a guaranteed lifetime income:

- Certainty of locking in a known rate at the time of starting the investment, with guaranteed annual increases every year an investor waits to access their lifetime income

- Certainty of receiving guaranteed income payments for life – however long that may be, thus mitigating longevity risk

- Certainty of having investments partially or fully protected against market downturns while in the Growth Phase, and fully protected in the Lifetime Income Phase, thus mitigating market and sequencing risk

- Certainty of having access to the investment value at any time to cover unplanned expenses

- Certainty of having beneficiaries receive the investment value in the event of death

Conclusion

In the same way that investment and insurance philosophies are foundational resources for advisers and advice practices, driving more efficiency and consistency and quality outcomes for clients, the time is now right for the Retirement Income Philosophy concept to become mainstream.

It is recommended that at the very least, a formal Retirement Income Philosophy should codify the practice beliefs and preferences around:

- The risks faced in retirement

- The methodologies to assess those risks

- The strategies that align income needs with individual client risk profile, and

- The product solutions used to implement those strategies.

Having examined why the risk methodologies commonly used in accumulation are inappropriate and problematic in decumulation scenarios, this paper proposes a new approach which recognises the importance of income certainty. This new approach includes new ways to more holistically assess a client’s preferred retirement income ‘style’, and the new generation of retirement income stream product solutions that can bring strategies to life.

If you would like to have PDF copy of this document, click here.

References

- Retirement Income Covenant a win for advisers – but for how long?

- Australian super system slips down global index

- Information report Implementation of the retirement income covenant: Findings from the APRA and ASIC thematic review

- Retirement and Retirement Intentions, Australia

- CPD: The most significant retirement risk of them all

- Managing retirement income with a bucket strategy

- What is Different about Decumulation?

- Longevity the Uncertainty and Managing the Risks

- An update on superannuation account balances

- Health sector has third highest inflation in Australia: ABS

- Pensioners experience higher increases in living costs

- Are you paying tax by not starting a super pension?

- ‘Grey divorce’ on the rise as third of Australian couples over 50 separate

- CPD: The most significant retirement risk of them all

- Retirees’ Needs and Their (In)Tolerance for Risk

- ASX AUSTRALIAN INVESTOR STUDY 2023

- Assessing customer risk profiles at retirement requires a dedicated tool

- Assessing customer risk profiles at retirement requires a dedicated tool

- Why Risk Tolerance Questionnaires Don’t Work for Determining Retirement Strategies

- Undertaking cashflow modelling to demonstrate suitability of retirement-related advice

- Why Certainty Is So Important In Retirement

- Actuaries develop a framework for maximising retirement income