The Problem in today’s Advice Market:

We all know that the great majority of working Australians cannot afford the increasing cost of traditional comprehensive advice.

We call that the ’advice affordability gap’ and it impacts approximately 10.4 million working Australians who have unmet advice needs. As well as these unmet needs, we know:

• The lack of affordability means that 90% of customers seeking advice are willing to pay less than $700 for advice

• The current adviser numbers do not provide adequate capacity at the right price to service these clients.

The Solution utilised by advisers to solve the Problem:

To solve this problem, FinTech’s have taken the traditional financial advice model and digitised the process by rethinking the way we use technology and creating digital journey’s which deliver affordable, compliant single topic advice – with the option to engage with a human, i.e. the ‘Hybrid Advice’ option.

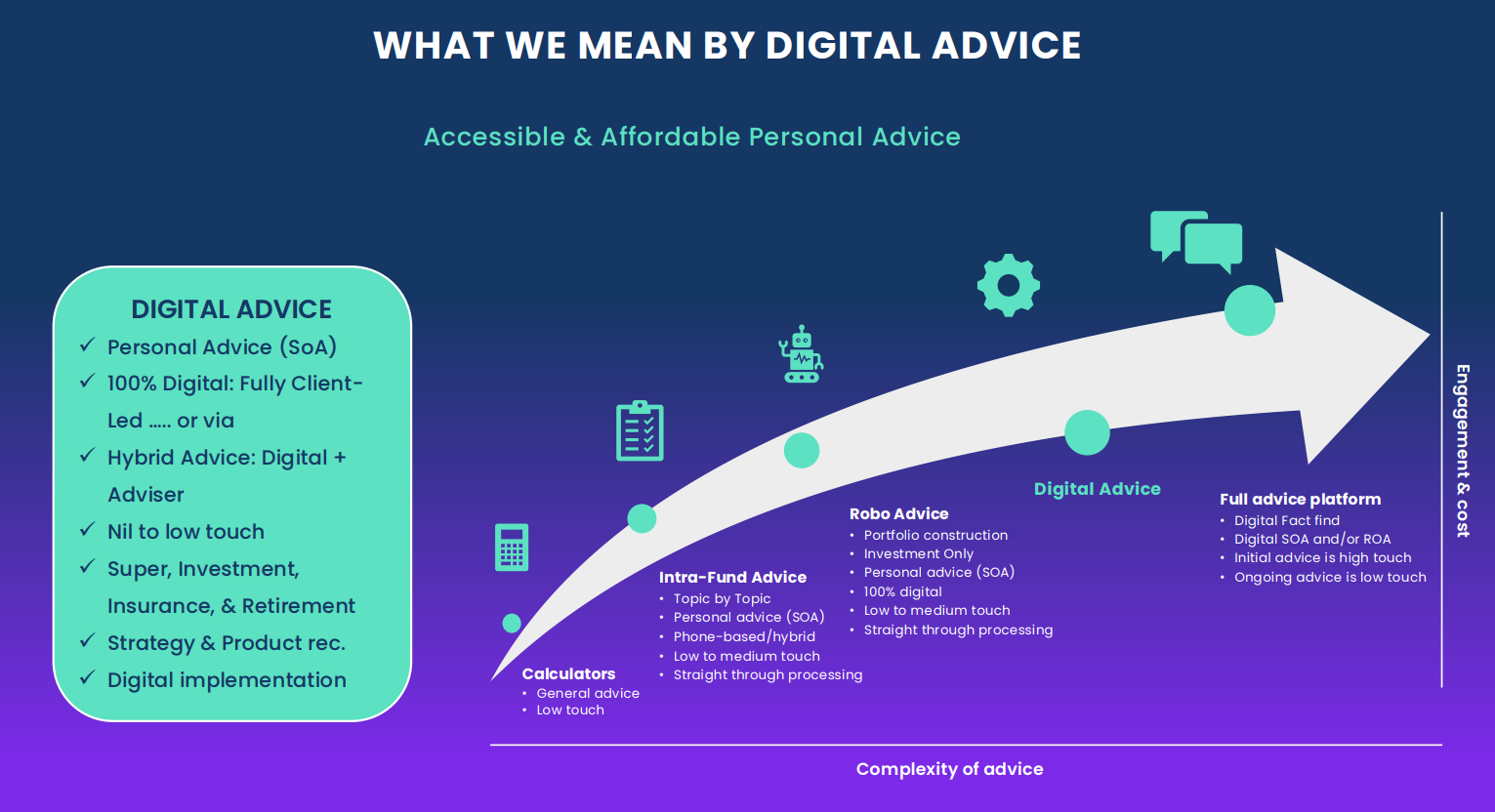

Whist the digital advice process used varies between providers, a typical advice journey can be undertaken as follows:

• Client completes digital fact-find that reviews their situation to determine the most appropriate advice topics for their financial position, and which are also in their Best Interest.

• The Fintech’s algorithm and ‘advice decision making rules’ perform calculations and trade-offs to provide advice recommendations. As digital advice is a rules driven industry, it is the algorithm and not AI that is used to determine the advice recommendations.

• The process should offer both strategy and product recommendations across; super, investment, insurance, retirement if possible, as clients need a complete solution. This differs from ‘robo-advice’ offerings – which only cover investment advice.

• Integrations with external providers can be used to pre-populate parts of the fact-find and ensure quality data is captured.

• As a result the client can engage in a fully digital experience from start to finish – including implementation.

The trend to offering ‘Hybrid Advice’: The Game Changing combination of Human Expertise & Digital Technology

There is a clear trend for clients to be reassured they are progressing their digital journey as they should – by having contact with humans. This digital-human or ‘Hybrid Advice’ model is now the preferred client experience and can be supported by the financial adviser or their support staff.

The ‘Hybrid Advice’ model adds a sense of security for clients, which is important given that for most, it is their first foray into financial advice. Given this, digital platforms should identify clients who may need comprehensive advice and triage them to their respective financial adviser as part of this process.

Some compliance items to consider in this process include:

• Clients should be able to complete all compliance requirements digitally including KYC /AML-CTF obligations and letters of engagement.

• The final item to consider is under whose AFSL is the digital advice being offered – the digital providers or the advisers.

Chart 1: What We Mean By Digital Advice

Which client cohort is best suited to use Digital Advice services?

The client cohorts ideal to use digital advice are categorised into two key groups:

Group 1: Representing clients such as: Millennials, Digitally Savvy, Non-advised, Insurance only, Children of HNW, Employees via corporate super, can access topics to help them establish their financial foundations as early as possible. Financial education services also play a key role in helping clients improve their financial literacy.

Group 2: Representing clients who are considering retirement. Advice technology now caters for this group by offering topics covering: Retirement income, TTR and a growing suite of Superannuation topics at affordable prices.

How best to integrate a digital advice proposition into a financial planning practice

Key considerations on how to successfully integrate a digital advice solution into a financial planning practice include:

• Client segmentation: This service is for the client cohorts already identified in Groups 1 & 2. However some advisers are adopting the use of the digital fact-finds to establish a picture of a client in a very time efficient and cost-effective way as a starting point for their advice relationship.

• Services integrations: These will depend on the digital provider and may include – Open banking and integrations with industry CRM’s

• Operational capability: Integrating a digital solution – including staff training, should have little if any impact on the businesses operational activities.

• Marketing: The digital provider may also provide a full service or ‘turn-key’ offering, including a standard marketing program, to service a specific client group.

• Referral Partner integrations: One of the key attributes of good tech, is that it allows you to scale your business – quickly, cost effectively and with improved productivity. Digital advice platforms can be integrated into referral partner businesses – such as accounting firms or mortgage brokers, providing access to a significant number of client opportunities – including identifying complex advice needs.

The Digital Advice Solutions ROI

Access to digital advice platforms is usually undertaken via a subscription fee (i.e., monthly, or annual) which range from less than $1.0k pm, i.e., in simple terms the cost of approx. 2-3 full SoAs pa!

The service can be white-labelled, integrate the advisers in-house services (i.e. insurance, lending, and full advice) and in some cases documents can be branded.

Digital providers can also offer single topic advice SoAs for less than $300 per topic, making it a very affordable exercise for the end client and an incredibly positive value proposition for any advice practice.

The Benefits To An Adviser of Digital Advice Technology

Incorporating a digital advice offering into a practice can greatly benefit the advice business in many ways, such as:

• Digital advice allows an adviser to more sustainably service clients with; lower balances, and have simple needs

• Advisors can scale their business with little effort or cost to service a market they cannot afford to reach now, giving them more time with existing clients & makes them more money — by ‘Stealth’.

• Establish a ‘white-label’ branded digital advice platform using the digital providers AFSL.

• Maintain Relationships with Non-advised, orphaned, millennials, employees, individual tax & SME’s — the advisers future HNW clients.

• Attract new clients: Digitally savvy and children of existing HNW — the advisers future HNW clients.

• Identify more full-advice clients.

• Engage referral partners more effectively and with scale.

• Improve the advisers bottom line and overall business value.

To learn more about how the Money GPS digital advice offering can help your business, visit our website or contact CEO & Co-founder George Haramis on: 0410 590 526 or george@moneygps.com.au

REFERENCE

1. Median fee of full financial plan @ $4.50k Investment Trends 2023