Key points:

• Advisers are expecting another strong run in global equities this year, with rate cuts in full swing across developed markets

• Advisers see further upside in the US, as robust economic growth and a broadening set of ‘winners’ looks set to drive gains in the S&P 500 and beyond to mid and small-caps

• Technology is the sector of choice once again in 2025, with advisers bullish on its long-term prospects despite stretched valuations

2024 was the year of the equity market rally that could. Despite pockets of (often extreme) volatility over the course of the year, both local and global shares overcame investor nerves around the macro outlook to generate solid returns.

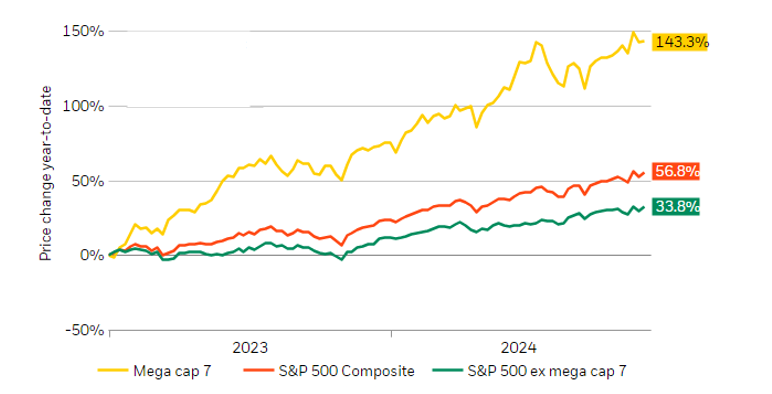

Yet if we take a closer look at where the growth came from last year, it’s undoubtedly US equities, and technology in particular, that powered markets to a strong finish. The S&P 500 achieved a more than 23% return in 2024, narrowly behind 2023’s result and the first time since the late 1990s that the index has achieved consecutive gains of more than 20%.1

Source: LSEG Datastream, BlackRock Investment Institute. Nov 27, 2024. Notes: Mega cap 7 includes Apple, Microsoft, Google, Amazon, Meta, Nvidia and Tesla. This is not a recommendation to invest in any particular financial product.

This unprecedented result has led some to question how much longer the rally in tech can continue, with the sector now making up more than 30% of the MSCI World Index’s total market cap – the highest market share since the dot-com bubble in early 2000.2 But with earnings continuing to deliver, and global AI-related investment just getting started, we still see a lot of upside in both AI and US equities more broadly – and so do advisers.

Below, we identify the four key themes advisers have told us are key to their thinking when it comes to client portfolios this year, from the broader market outlook to what sectors and asset classes are capturing their interest.

1. The risk-on rally continues

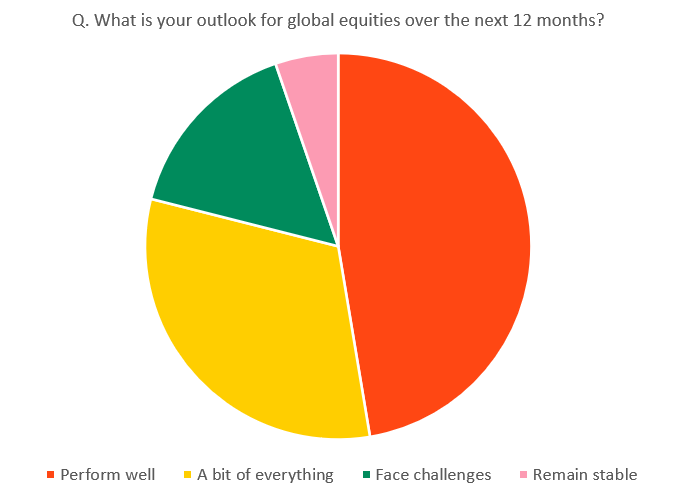

In our first quarterly pulse survey conducted in Q4 2024, a significant proportion of advisers said they expected global equity markets to perform well this year, with just a handful pointing to mixed or challenged performance. This echoes our house view on markets this year – with interest rates now falling across most developed markets, we see a positive outlook for risk assets and prefer equities over bonds.

Source: BlackRock Quarterly Pulse Survey data as at 26 November 2024

As the possibility of a ‘hard landing’ from high interest rates and inflation looks ever less likely, we’re instead leaning into a scenario of moderate global growth and a market environment that continues to be led by US corporate strength, technology and other winners from the AI revolution. The outlook for fixed income, and for bonds’ traditional role as a portfolio diversifier, is less certain given the persistent government deficits we are likely to see in Australia and globally.

2. Opportunities in US exceptionalism

Advisers are also confident that the US equity rally will continue this year, with most pointing to the US as the market they’re most interested in increasing allocations to, while a few are also keen on adding to Australian equities. Indeed, despite stretched valuations both historically and relative to other developed markets, we believe the US is poised to keep outperforming given its deep exposure to the AI theme and positive economic fundamentals.

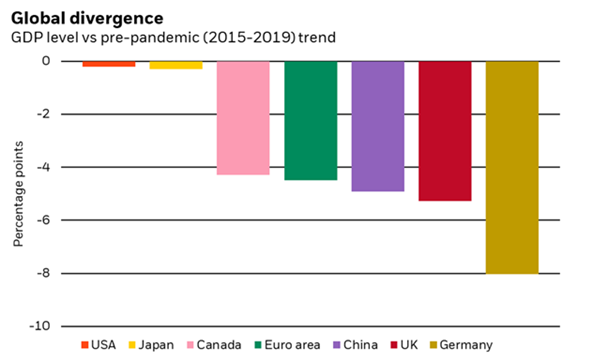

Taking a look at economic growth across different global markets, we can see that the US and Japan stand out as the only economies where GDP is returning to pre-pandemic trend levels (see chart below). With US earnings growth also broadening out from a concentrated technology scenario to other sectors including financials, utilities and materials, we expect to see a broader set of winners across corporate America in the coming year.

Currency is also an important consideration for investing in the US, and with a host of macroeconomic variables set to potentially impact the outlook for the USD-AUD exchange rate – including tariffs, interest rate movements and stimulus in China – advisers may want to consider hedged exposures.

3. A transformative moment in markets

When it comes to the winning sectors this year, advisers are still pretty confident on technology. The majority of those who responded to our pulse survey pointed to tech as the potential biggest gainer in 2025, with a handful of votes for the more defensive sectors of healthcare and consumer staples.

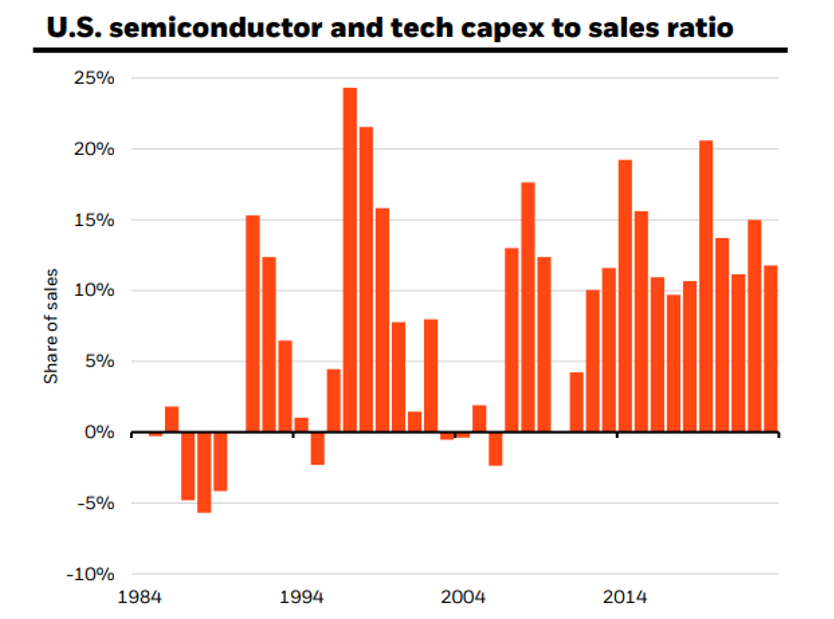

This may be somewhat surprising given the outsized performance we’ve already seen in tech over the past couple of years3– but not when you consider that we may only be at the first phase of a long-term AI ‘megaforce’ that will transform the global economy. With 10% of all semiconductor and technology sector sales currently reinvested into capital expenditure, product innovation and growth in the AI space is likely to expand from here.

It is not possible to invest directly in an index. Indexes are unmanaged. Index performance does not account for fees.

Source: BlackRock Investment Institute, with data from LSEG Datastream, October 2024. Notes: The chart shows the capital expenditure (capex.) of the US semiconductor and tech sectors relative to their sales. We use index proxies for sectors constructed by Datastream – US DS Semiconductors and US DS Technology.

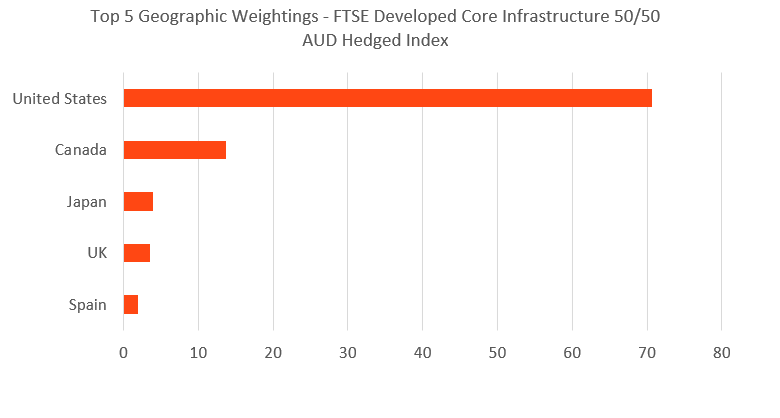

4. Diversify your diversifiers

Another key trend that’s come up in conversations with advisers over the last year is adding diversification for when those pockets of equity market volatility occur. With bonds not providing as much of a cushion against equity market shocks as they used to, advisers are interested in looking further afield for asset classes with a low correlation to equities.

Source: FTSE Russell as at 31 October 2024.

Source: FTSE Russell as at 31 October 2024. This is not a recommendation to invest in any particular financial product.

Global listed infrastructure and global property are two sectors that fit this bill, and are also set to benefit from US and AI-related tailwinds, with significant weightings to US equities and data centre providers (see above charts). With geopolitical tensions likely to continue this year, we also see an expanding role for gold as a hedge against uncertainty and think central bank demand will be supportive of further price rises.

Overall, it seems advisers are positioning for further, concentrated gains in equity markets this year – while exploring how they can build more resilience in their portfolios longer-term.

BlackRock’s Wealth Symposium is back for 2025!

Join us for these half-day events, designed to bring together industry peers to discuss, share, and inspire solutions that not only meet today’s challenges but will carry through as the industry transforms. The line-up of international guests and local experts will offer a unique opportunity to network, learn, and collaborate. Click your city to find out more and register: Melbourne, Brisbane, Sydney.

Opinions are subject to change and they are not a guarantee of future results. This information should not be relied upon as research, investment advice or a recommendation.

References

1. Source: Bloomberg, 31 December 2024. Past performance is not a reliable indicator of future performance.

2. Source: BlackRock/LSEG Datastream data as of 25 November 2024.

3. Source: BlackRock/LSEG Datastream data as of 26 November 2024. Based on performance of Magnificent 7 vs broader S&P 500 Index

IMPORTANT INFORMATION

Issued by BlackRock Investment Management (Australia) Limited ABN 13 006 165 975, AFSL 230 523 (BIMAL) for the exclusive use of the recipient, which warrants by receipt of this material that it is a wholesale client as defined under the Australian Corporations Act 2001 (Cth).

This material provides general advice only and does not take into account your individual objectives, financial situation, needs or circumstances. Before making any investment decision, you should assess whether the material is appropriate for you and obtain financial advice tailored to you having regard to your individual objectives, financial situation, needs and circumstances. Refer to BIMAL’s Financial Services Guide on its website for more information. This material is not a financial product recommendation or an offer or solicitation with respect to the purchase or sale of any financial product in any jurisdiction.

Information provided is for illustrative and informational purposes and is subject to change. It has not been approved by any regulator.

This material is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. BIMAL is a part of the global BlackRock Group which comprises of financial product issuers and investment managers around the world. BIMAL is the issuer of financial products and acts as an investment manager in Australia.

For BIMAL Schemes: BIMAL is the responsible entity and issuer of units in the Australian domiciled managed investment schemes referred to in this material, including the Australian domiciled iShares ETFs. Any potential investor should consider the latest product disclosure statement (PDS) before deciding whether to acquire, or continue to hold, an investment in any BlackRock fund. BlackRock has also issued a target market determination (TMD) that describes the class of consumers that comprises the target market for each BlackRock fund and matters relevant to their distribution and review. The PDS and the TMD can be obtained by contacting the BIMAL Client Services Centre on 1300 366 100. In some instances the PDS and the TMD are also available on the BIMAL website at www.blackrock.com/au. An iShares ETF is not sponsored, endorsed, issued, sold or promoted by the provider of the index which a particular iShares ETF seeks to track. No index provider makes any representation regarding the advisability of investing in the iShares ETFs. Further information on the index providers can be found in the BIMAL website terms and conditions at www.blackrock.com/au.

BIMAL, its officers, employees and agents believe that the information in this material and the sources on which it is based (which may be sourced from third parties) are correct as at the date of publication. While every care has been taken in the preparation of this material, no warranty of accuracy or reliability is given and no responsibility for the information is accepted by BIMAL, its officers, employees or agents. Except where contrary to law, BIMAL excludes all liability for this information.

Any investment is subject to investment risk, including delays on the payment of withdrawal proceeds and the loss of income or the principal invested. While any forecasts, estimates and opinions in this material are made on a reasonable basis, actual future results and operations may differ materially from the forecasts, estimates and opinions set out in this material. No guarantee as to the repayment of capital or the performance of any product or rate of return referred to in this material is made by BIMAL or any entity in the BlackRock group of companies.

No part of this material may be reproduced or distributed in any manner without the prior written permission of BIMAL.

© 2025 BlackRock, Inc. or its affiliates. All Rights reserved. BLACKROCK, BLACKROCK SOLUTIONS, ALADDIN, iSHARES and the stylised i logo are registered and unregistered trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners. MKTGH0125A/S-4171181