In a world of overwhelming financial choice and volatile markets, even the best-designed portfolio can fall short — not due to poor structure, but poor investor behaviour. Panic selling, misaligned expectations, and overreaction to short-term movements are not just market problems; they’re behavioural ones. Solving this requires a two pronged approach; goal-based compartmentalisation layered on top of risk-defined investment strategies.

On their own, each approach offers value. Together, they deliver something far more powerful: a behavioural framework that not only performs, but endures.

Part 1: Compartmentalisation – Giving the Mind a Map

Clients don’t think in Sharpe ratios or correlation metrices — they think in stories, timelines, and goals. They organise their financial lives in mental silos: “This is for the kids’ education,”

“This is my safety net,” “This is for travel once I retire.”

This isn’t irrational — it’s a behavioural reality known as mental accounting. While traditional finance treats all dollars as equal, behavioural finance recognises that context shapes perception.

By deliberately compartmentalising portfolios into goal-aligned buckets, we help clients:

• Reduce decision fatigue by clearly linking investments to purpose

• Experience less regret aversion by contextualising drawdowns

• Gain psychological ownership through labelled goals and intuitive framing

When goals are explicit, investors are less reactive and more patient. A drawdown in a “20-year retirement bucket” feels very different than a drop in an all-in-one unlabelled portfolio. That shift in framing often makes the difference between staying invested and pulling the pin.

Part 2: Risk Design – Engineering Robust, Transparent Exposure

Of course, psychological framing alone doesn’t manage downside risk. For that, we need precision.

Risk-defined portfolio construction ensures each bucket is matched to an appropriate exposure, tailored to:

• Time horizon

• Drawdown tolerance

• Required return

• Liquidity needs

Rather than relying on blunt labels like “Balanced” or “Growth,” this approach defines portfolios by their volatility parameters, exposure limits, and structural resilience.

This risk engine provides the chassis beneath the compartmentalised design. With clearly articulated risk bands, clients can understand what each compartment is built to do — and what it isn’t. That clarity builds trust and reduces surprises.

And when unexpected events do occur? Risk-based construction ensures drawdowns remain within guardrails, reducing the likelihood of emotionally triggered exits.

Part 3: The One-Two Punch – Why Both Matter Together

The genius lies in the interplay. Neither framing nor engineering is sufficient in isolation.

• A compartmentalised plan without risk alignment might feel intuitive but collapse under volatility.

• A risk-engineered plan without behavioural framing might perform well on paper but fail in the real world, where perception drives behaviour.

Together, they create psychological safety and mechanical resilience. When clients know why they own something, what it’s for, and how it behaves, their ability to stay the course improves dramatically.

We’ve seen this firsthand. Clients with well-labelled, risk-calibrated compartments:

• Made fewer portfolio changes during the early 2020 COVID market crash

• Rebounded more quickly after poor bond returns in 2022–23

• Expressed greater satisfaction and understanding in review meetings

Their outcomes weren’t just better — they were more durable.

Part 4: Behavioural Validation – The Science Behind the Structure

This approach draws from a range of well-documented behavioural concepts:

Mental Accounting

Coined by Richard Thaler, this principle explains why people treat money differently based on its label or intended purpose. Matching investment buckets to natural mental accounts creates alignment, not friction.

Framing Effect

Clients interpret identical facts differently depending on presentation. Calling a portfolio “your future income stream” versus “a balanced fund” produces materially different responses to volatility.

Loss Aversion

People feel the pain of losses twice as strongly as they enjoy gains. Bucketing helps buffer this by separating drawdowns in non-critical or long-term compartments from essential capital.

Endowment Effect

When clients perceive a portfolio as “theirs,” they are more likely to protect it and less likely to abandon it. Framing compartments as dedicated to a personal goal triggers this effect.

Regret Minimisation

When expectations are framed up front — with clarity about purpose and risk — there is less room for hindsight regret. This reduces second-guessing and adviser blame during downturns.Together, these effects act as behavioural guardrails. They don’t eliminate emotion, but they channel it into more productive directions.

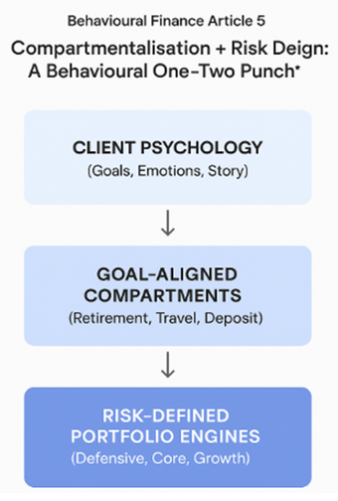

Part 5: Visual Summary – How the Framework Fits Together

Here is a plain-text diagram of how compartmentalisation and risk design interlock within the portfolio structure:

Each level builds upon the one below:

• The base layer delivers structural resilience through calibrated risk.

• The middle layer organises investments by purpose and timeline.

• The top layer connects the plan to human emotion — where confidence and decisionmaking live.

This structure allows for tailored conversations, precise planning, and emotionally resilient behaviour.

Most advisers know that client behaviour is often the biggest driver of long-term outcomes. But few tools are designed to actively shape that behaviour for the better.

By combining goal-aligned compartmentalisation with precision risk design, advisers can:

• Frame conversations in language that builds trust

• Align structure with psychology

• Reduce panic-switching during market stress

• Increase adherence and retention

• Deliver investment experiences that make sense — and feel right

This isn’t a sales tactic. It’s a strategy grounded in science, refined by experience, and made real by structure.

Innova’s behavioural design philosophy is simple:

Help clients understand it. Help them stay the course. Help them succeed

To receive 0.25 Technical Competence CPD points for this article, complete the quiz here.

Important Information

This document has been prepared by Innova Asset Management Pty Ltd, ABN 99 141 597 104, which is a Corporate Authorised Representative of Innova Investment Management, AFSL 509578.

The information contained in this document is commentary only. It is not intended to be, nor should it be construed as, investment advice. The views expressed are subject to change at any time based on market and other conditions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Before making any investment decision you need to consider your particular investment needs, objectives and financial circumstances.